Forced displacement is one of the most pressing challenges of our time. With the number of forcibly displaced estimated at nearly 71 million in 2018, the scale of the crisis is impeding progress towards achieving UN Sustainable Development Goals as well as commitments to “leave no one behind”. The protracted and complex nature of forced displacement requires that urgent life-saving humanitarian support be complemented by development action.

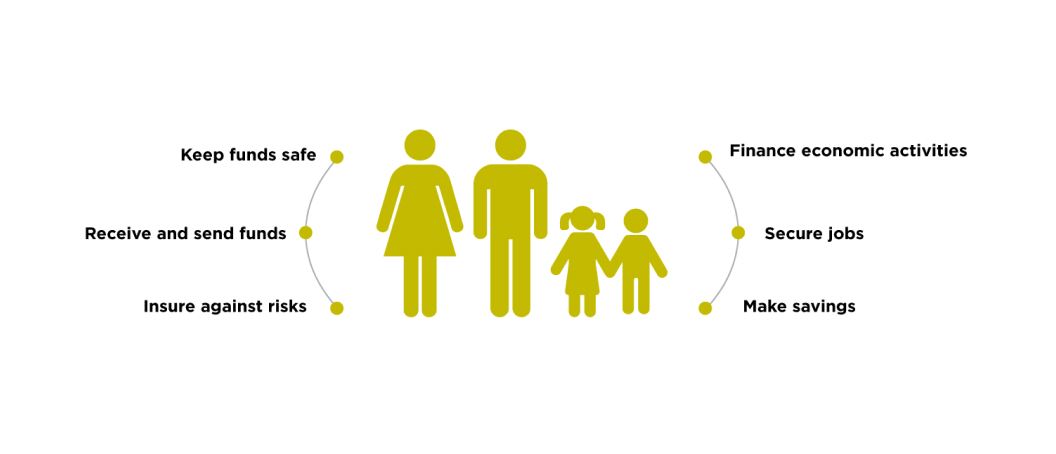

Financial inclusion empowers forcibly displaced persons (FDPs) to cope under extremely difficult circumstances while also meeting their broader, long-term financial needs. Access to formal financial services creates conditions for FDPs to establish coping mechanisms, build self-reliance and resilience, apply their skills and competencies, restore their livelihoods, and realise their full potential. In turn, they can contribute to the economic growth of their host country, voluntarily return home or resettle in a third country.

Specific challenges in advancing policy and regulation for the financial inclusion of FDPs include:

AFI supports peer-to-peer learning on financial inclusion initiatives that can offer the same opportunities for FDPs as other country residents but only when adapted and applied appropriately. Successful programs and best practices indicate that it is necessary to tailor approaches while taking the FDP context into account and adding complementary services where needed.

Financial policymakers and regulators in emerging economies are taking significant steps to adopt innovative regulatory approaches in order to financially include FDPs. In the past year, several AFI members, such as Central Bank of Mauritania, Da Afghanistan Bank and National Bank of Rwanda, implemented policy and regulatory reforms that enhanced access to formal finance for FDPs living within their jurisdictions. This is in addition to efforts by other members, including Bank of Tanzania, Bank of Zambia, Bank of Uganda and Central Bank of Jordan, which have championed this issue for several years now.

Snapshot of the Forcibly Displaced Persons activities within AFI:

| 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|

| Standalone Events and/ or Sessions |

GPF session The long road travelled – Inclusive Finance for Refugees |

GPF session Transforming the lives of Forcibly Displaced Persons (FDPs) through financial inclusion |

GPF session Digital Identity – A Financial Inclusion Revolution for the Most Vulnerable Populations |

GPF session Technology is the Key to Youth Financial Inclusion |

| Knowledge Products (aggregate) |

0 | 1 | 1 | 2 |

| Policy Changes (aggregate) |

0 | 0 | 0 | 0 |

| Peer Reviews (aggregate) |

0 | 0 | 0 | 0 |

Financial regulators and policymakers can drive, influence, and facilitate efforts to design and offer formal financial services to FDPs by creating an enabling regulatory environment that fosters innovation yet still ensures sound compliance.

© Alliance for Financial Inclusion 2009-2024

About

About

Online

Online

Data

Data