27 May 2016

Account Ownership in AFI Member Countries Reveals Some Surprises

Account ownership is widely recognized as a first step toward financial inclusion. The Global Findex defines account ownership as “having an account either at a financial institution or through a mobile money provider.” Levels of account ownership vary across AFI member countries, and after digging into data on 70 of these countries, I uncovered some exciting facts behind these differences.

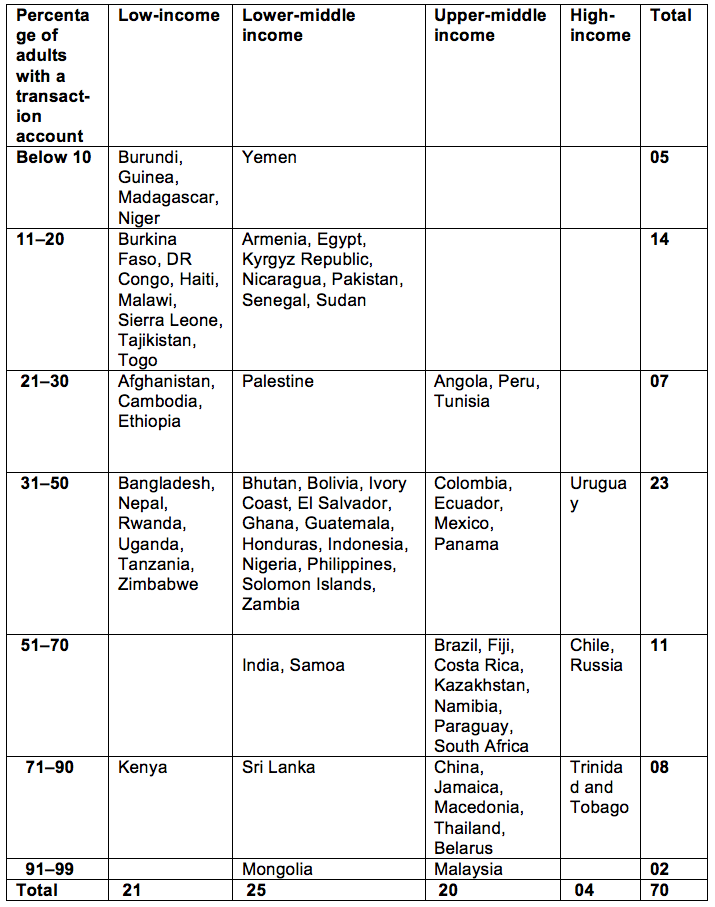

First, there is tremendous diversity across AFI member countries in the level of account ownership, ranging from 6.4% in Niger to 91.8% in Mongolia. Although this is not the most surprising finding, what is interesting is that these differences were evident across low-, middle-, and high-income groups and within each of these groups, too.

Second, in 21 of the 70 countries, 51% or more of adults owned accounts. In 10 of the countries, account ownership reached or topped 71%, perhaps the highest levels in the AFI Network in 2014. Kenya stands out as the only low-income country to have more than 71% account ownership — all the others were lower- or upper-middle income countries. Kenya’s outlier status suggests that a low income level may not necessarily be a barrier to achieving a relatively high level of account ownership. Another interesting finding was that only Malaysia and Mongolia had account ownership levels exceeding 91% at the end of 2014.

Third, six of the 10 countries with a high level of account ownership (71% or higher) were classified as upper-middle income, while only one high-income member institution country, (Trinidad and Tobago) and two lower-middle income countries (Sri Lanka and Mongolia) fell into this category.

Fourth, account ownership was very low (below 10%) in only five of the 70 countries studied. Four were low-income from the Sub-Saharan African region, while the other was a lower-middle income country from the Middle East and North Africa region (Yemen). Also notable was that only four of the 21 low-income countries had account ownership levels below 10%.

Fifth, in 49 (70%) of the 70 countries, account ownership was 50% or less. Approximately 43% of these were lower-middle income countries.

Overall, the data seems to suggest that some countries have been able to dilute the negative impact of low income on account ownership through smart policies and strategic approaches. This reaffirms the critical role AFI could play in advancing both account ownership and financial inclusion at the country level.

Table: Level of financial inclusion by income group in 70 AFI member countries (2014)

ABOUT THE AUTHOR

Nimal Fernando is a consultant at the Alliance for Financial Inclusion.

© Alliance for Financial Inclusion 2009-2025

About

About

Online

Online

Data

Data