27 January 2016

Assessing the key takeaways from Samoa’s financial services demand side survey

Located in the South Pacific region with a population of less than 200,000, Samoa is a small, open economy with a narrow export base heavily dependent on remittances. It is one of the two Pacific Island economies in the list of top 10 remittance recipients as a percentage of GDP. This has huge economic and social implications from the household to the macro level.

In the context of financial inclusion, Central Bank of Samoa (CBS) has taken a lead role in collaborating with key stakeholders in creating an enabling regulatory environment in facilitating access to finance for underserved and unbanked sections of economy. To have a better understanding of the financial inclusion landscape in Samoa, CBS in partnership with the Pacific Financial Inclusion Programme (PFIP) and the Alliance for Financial Inclusion (AFI) undertook a national demand side survey in 2015.

The sample size for this national survey was 963.

Snapshot: Key highlights

1. There is higher proportion of women who are financially included in comparison to men.

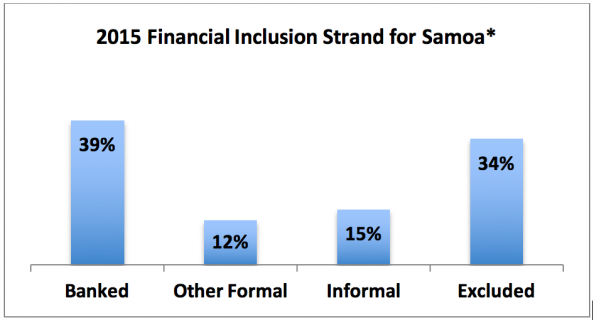

In Samoa, 66 percent of adults have some form of financial products and services. In terms of gender breakdown, there are 40 percent of women who have a bank account when compared to 38 percent of men. Similarly, 13 percent of women also use other formal financial services in comparison to 11 percent of men, and 17 percent of women access informal financial services in comparison to 12 percent of men. On the other hand, 39 percent of men are completely excluded from financial services compared to 30 percent of women.

2. Barriers to access and usage of financial services and products are still prevalent more in rural areas.

While the majority of the unbanked Samoans attribute lack of money as the reason for not having a bank account, other key factors among the financially excluded population (mostly associated with rural segment of population) included: distance to financial access point; minimum balance required to open an account; and the average waiting time to get a transaction done.

3. To a greater extent, it can be inferred that there is a positive relationship between receiving remittances and having a bank account.

There is a significant proportion of population (particularly women) that receive remittances on a daily basis with most of these funds are used to cover daily expenses. New Zealand is the major source of remittances for Samoans. Out of those adults that receive remittance income, 42 percent are currently banked and 22 percent have also been previously banked at one point in time.

4. Similar to other Pacific Island economies, Samoa also has a low uptake of mobile financial services.

While 71 percent of adults own a mobile phone, only 3.7 percent of mobile phone owners have a mobile money account. It is also interesting to note that the cost of sending remittances through a mobile phone is competitive in terms of cost and duration of transfer, however, most Samoans still prefer to use expensive alternatives.

Way Forward: Opportunities for Growth

1. Financial literacy training specific to mobile financial services.

Due to the geographic locations of a number of communities in Samoa, accessibility to financial services and products continue to be a barrier. Emergence of mobile financial services was perceived to be the solution to this problem. However, this innovative means of transacting has not been positively received in Samoa as it was anticipated and majority of the population do not know what this system is all about. Thus, there is need for more awareness and guidance on the benefits and use of this platform.

2. Need for more remittance-linked financial products.

In comparison to Fiji and Solomon Islands, Samoans tend to save less. There is scope for introducing remittance-linked savings products that encourages remittances recipients to save a proportion of income for other productive purposes. Financial literacy training among the recipients can also assist in this goal.

3. Youths as a locomotive for innovation and financial inclusion.

The survey highlighted that 70 percent of adults aged 15-20 and 30 percent of adults aged 21-30 are excluded from financial services entirely. This indicates that there is an urgent need to mainstream youths into the financial inclusion agenda. Financial service providers in Samoa need to build capacity to offer youth viable, customized and quality financial services. Financial education in schools needs to be supplemented with real life learning to ensure a smooth transition from childhood to adulthood.

* For the purpose of this Survey, the following definitions were used: Banked – the respondent currently has a formal bank account; Other Formal – over the past 12 months, the respondent used the services of a credit union, microfinance institution, the Samoa National Provident Fund, investments, or insurance; Informal – over the past 12 months, the respondent has used a savings club or other non-regulated financial instrument, such as taking credit from a moneylender, shop or hire purchase; and Excluded – over the past 12 months, the respondent has not used any of the services mentioned for the other three categories, but may have borrowed from or lent to friends and family, saved money in the house, pawned goods, borrowed from an employer, saved with a money guard, or trusted person.

ABOUT THE AUTHORS

Lanna Lome-Ieremia is the Manager, Financial System Development at Central Bank of Samoa. Sameer Chand is a Senior Analyst at the Reserve Bank of Fiji.

© Alliance for Financial Inclusion 2009-2024

About

About

Online

Online

Data

Data