6 May 2016

Regulators innovating new approaches to SME finance

From the 24th to the 26th May, 2016, financial policymakers representing 26 countries from five continents, and high-level representatives from the Mongolian private and public sector will converge in Ulaanbaatar, Mongolia, for the 6th Small and Medium Enterprises Finance Working Group (SMEFWG) meeting. The meeting is expected to generate discussions on policy solutions to advance financial inclusion of small and medium enterprises (SMEs) across the AFI network. Furthermore, the meeting will allow regulators from the network to have an sights at the Mongolian experience and the great efforts conducted to include SMEs.

During the meeting, participants will work to finalize various knowledge products currently under development by AFI members. Those efforts include basic terminology, an outline of the most important and successful interventions to bring SMEs closer to the financial sector, and, discuss in-depth the role of the financial regulator to achieve the financial inclusion of SMEs.

Participants attending the meeting will have the opportunity to assess new topics related to SMEs and financial inclusion, such as agricultural finance for SMEs in the Philippines, India and across the globe; the relevance of digital payments in the value chain, and the relevance of creating infrastructure for SMEs. Mexico will also provide insights that will be commented by private sector actors MasterCard and the International Finance Corporation (IFC). The impact of financial stability on SMEs will be addressed regionally, and the Gender Dimension of SME finance policy-making will pose further steps to implement the Zero Draft AFI Action Plan for Gender and Women’s Financial Inclusion.

AFI member institutions will share their national insights, and set next steps to produce more knowledge if the topics referred above are prioritized. In this meeting, AFI will launch the AFI Data Portal—a unique financial inclusion repository of knowledge, discuss and formulate more commitments to achieve greater financial inclusion for SMEs under the AFI Maya Declaration, and, finally, participants will have the opportunity to tailor questions for the legal and regulatory repository of knowledge produced by the AFI network for the AFI Country Policy Profiles on SME Finance.

All of these efforts will showcase the value of the AFI network, and also raise a valid question: why financial policymakers from around the globe are discussing about smart policies to financially include SMEs? There are many reasons. The first is SMEs make an important contribution to employment and the increase of income level and the gross domestic product (GDP). As recently reported by the International Labor Organization (ILO), evidence shows that regardless of the economy size, SMEs have created 67% of the global employment and between 60-70% of the global GDP is attributable to SMEs (ILO, 2015, and World Bank, 2003).

AFI member institutions are aware of the importance of SMEs in the global economy, and precisely in this scenario, when looking at the biggest barriers faced by SMEs across countries, “access to finance appears” as a top constraint (IFC, 2013). In other words, access to finance is jeopardizing the growth and sustainability of SMEs, and also impeding the achievement of sustainable development and poverty alleviation. Under such a scenario, policymakers from the AFI network are working very hard to learn from each other under a south-to-south collaborative dialogue to find those smart policies that might bridge the gap for SMEs.

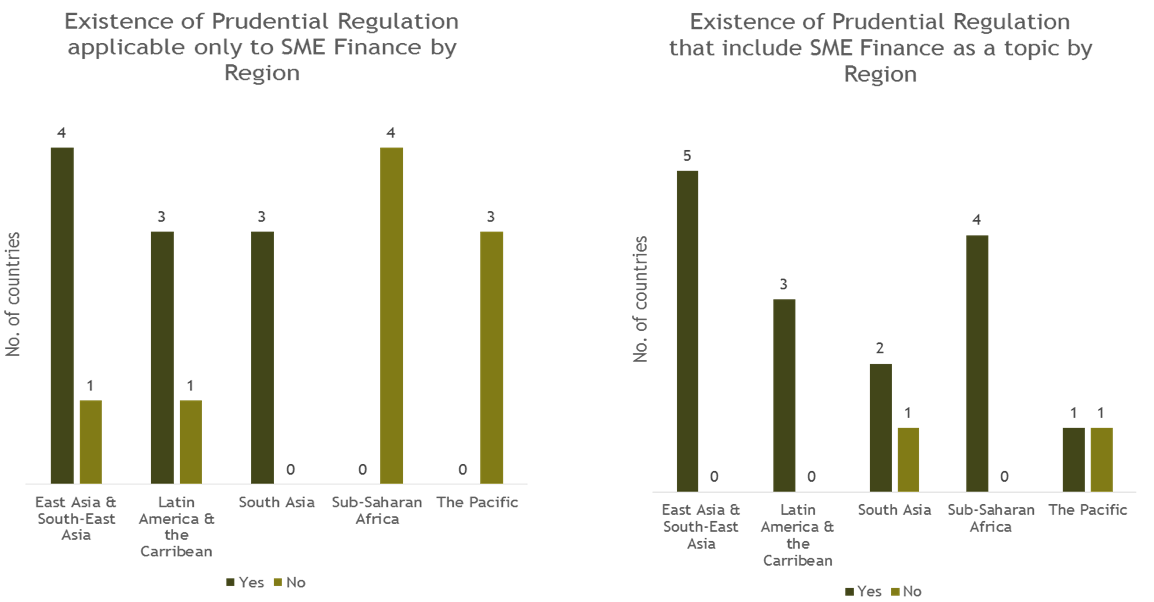

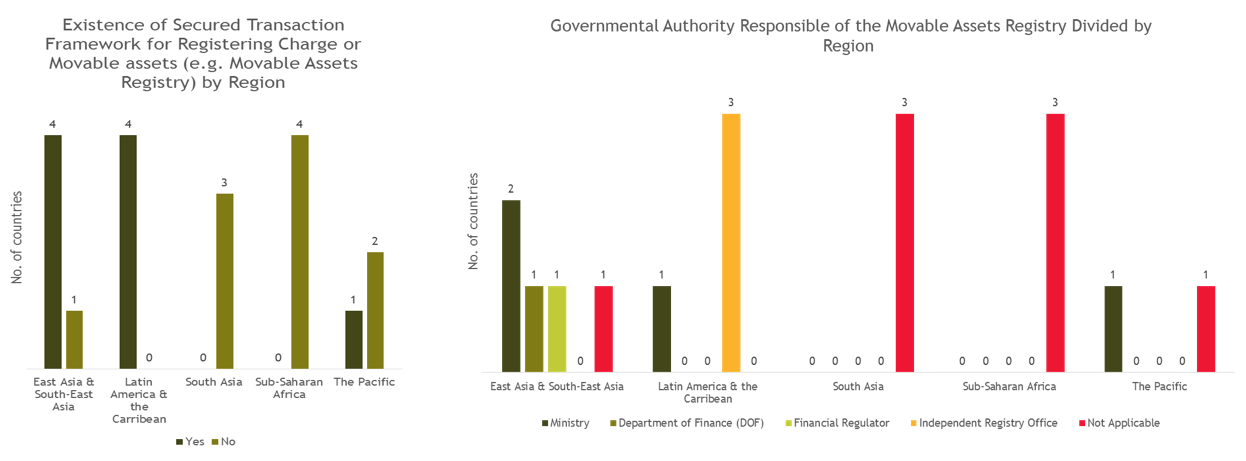

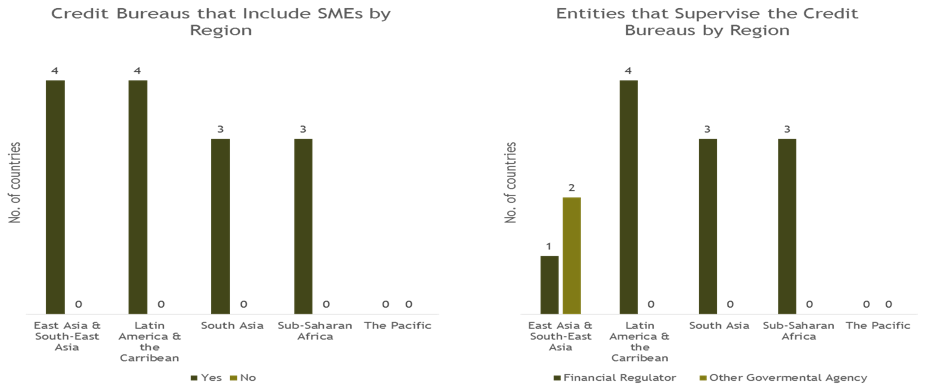

The SMEs gap also encompasses the finding of new policy solutions to include women, since the majority of SMEs are run by women across the globe. In other words, there is an inherent gender component when assessing SME finance policies. Considering this, the AFI SMEFWG conducted between 2015 and 2016 a survey to find evidence about the current status of SME finance policies. The survey contained 26 questions, responded by 19 countries from five different regions

These results are quite influential and show tangible evidence of the national level policy interventions to achieve greater financial inclusion, and also these constitute a baseline to assess the progress of the financial inclusion policies gauged to achieve greater financial inclusion.

SME Policy Interventions Summary

.png)

Considering carefully the findings of the survey, the group will use this input to inform its mandate and debate, as well as to finalize the knowledge products under progress. In any case, the evidence showcases that it is necessary to look upon the role of financial regulator, topic that will be discussed and clearly delineated in the meeting. As it might been seen, there is no a single role, and each country has different lessons to share and to discuss.

Financial policymakers are much focused on decreasing asymmetry of information between SMEs and the financial suppliers, and concerned about financial stability. Also, they have been active in the creation of financial capabilities and also to ensure the existence of infrastructure that bridges the current gap that prevents the access of SMEs to financial services. Specific regions and countries have been prone to be more active and involved in the establishment of quotas for allocating credits to SMEs, or creating cluster surveys by sector or by gender to entice private sector innovation and offering of funds in favor of SMEs.

The discussion is just getting started and the AFI network is working to bring smart financial inclusion policies to life for SMEs to achieve sustainable and inclusive development and poverty alleviation.

ABOUT THE AUTHOR

María del Rosario Moreno Sanchez is a Senior Policy Manager at the Alliance for Financial Inclusion. Follow her on Twitter at @marayaemese. Wong Wei Ping, Program Officer for Working Groups and Regional Initiatives at AFI, contributed to research for this blog.

© Alliance for Financial Inclusion 2009-2024

About

About

Online

Online

Data

Data